What Is Accounting Theory?

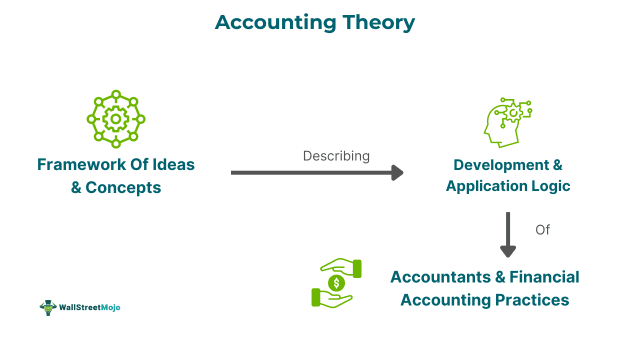

Accounting Theory refers to a framework of concepts and ideations that facilitate the applications and development of financial accounting practices. It guides the manner in which accounting data can be used to make business decisions, and transactions can be reported and recorded in financial statements.

You are free to use this image on your website, templates, etc.. Please provide us with an attribution link.

Financial accounting theory contains methodologies, assumptions, and frameworks to guide the execution and examination of financial principles. Financial accounting theory and analysis have been used to develop consistent standards of financial reporting. Moreover, it also ensures that financial data remains reliable, comparable, and relevant across entities.

Key Takeaways

- Accounting theory represents a framework of ideas and concepts aiding in the development and application of financial accounting procedures.

- It provides guidelines on how transactions should be reported and documented in financial statements. It also outlines how accounting data should be utilized to inform business decisions.

- Its types include the cost principle, matching principle, full disclosure principle, relevance, reliability, positive accounting theory, and mental accounting theory.

- It enhances decision-making, improves efficiency, and ensures compliance with economic laws and income tax regulations. Additionally, it logically justifies practices, simplifies audits, and helps accountants make informed decisions.

Examples

Let us use a few examples to understand the topic.

Example #1

A green energy company called Greena, located in Old York City and led by Mindy, recently acquired hi-tech innovative equipment. The total cost of this purchase was $600,000. Hence, as per the theory of cost principle, its transaction is recorded at its real cost price of $600000 in Greena’s financial records. Therefore, to align with the theory of the matching principle, Greena compares the expense of depreciation of $60000 every year with the profit generated by the hi-tech equipment.

Therefore, in the financial statements, Greena implements the theory of full disclosure by reporting an imminent lawsuit impacting its financial health and growth. Moreover, the relevance theory makes it possible that Greena’s financial reports focus on revenue growth. It does so with the help of its latest eco-friendly products vital to the decision of the investor. Finally, Greena complies with the theory of reliability by offering verifiable and accurate data, such as sales data of $3 million from its new product line. Hence, in this manner, it ascertains and creates trust in stakeholders to believe its financial data.

Example #2

An online article published on February 14, 2022, discusses a comment letter penned by students of public accountancy admitted into ACCT 440: Accounting Theory and Research. The letter addresses the 9 proposed edits to the Financial Accounting Standards Board (or FASB)’s interim report standard as published on its website. The assistant professor led groups of students in researching relevant problems and recommended that the suggested guidelines be used by financial statement users. They also provided additional suggestions based on their findings.

Christopher Shepp, acting as primary editor, co-authored the letter with 15 students. Furthermore, FASB would analyze all comment letters, organize public meetings for discussion, and conduct polls on the proposed new standard. As such, the project gave students valuable hands-on experience in developing accounting standards.

Importance

There are many reasons why this theory becomes important, as shown below:

- It aids in adding logic to accountants’ decision-making

- It facilitates the development of efficient accounting methodology within accountants

- Accounts can increase their efficiency by using it

- Ambiguity in practices of accounting can be reduced with its help

- It can logically justify the accounting practices

- It fosters planning and compliance related to economic laws and income tax

- It helps make the audit of accounts easier

- It plays a vital role in framing procedures and policies of accounting

- Interested parties can satisfactorily fulfill their informational needs in a better manner

- Accountants can come out of their dilemmas of choosing from various alternatives

- One can interpret and understand the accounting information from accounting documents in the best possible way.

Frequently Asked Questions (FAQs)

How to study accounting theory?

One can study the theory of accounting by focusing on methodologies, principles, and key frameworks guiding financial reporting. One can use online resources, textbooks, and academic journals to navigate the theory’s quantitative and qualitative aspects. After gaining a theoretical foundation, one can apply the knowledge to real-world situations to deepen understanding and practical skills.

What is normative accounting theory?

It focuses on setting of principles and guidelines regarding how accounting must be carried out as per moral and ethical. This approach emphasizes normative considerations rather than relying solely on empirical observations.

How is accounting theory related to accounting research?

Accounting research is grounded in conceptual frameworks and foundational principles of theory accounting. It is a vital element in advancing accounting practices and knowledge. It involves developing methodologies, interpreting financial data, and hypothesizing about it.

What are the classifications of accounting theory?

It can be classified into two main categories: positive theory and normative theory. Normative theory advocates ideal standards of accounting, while positive theory forecasts and explains actual principles of accounting. This classification facilitates the application and development of principles of accounting.