What Is Comparable Uncontrolled Price (CUP) Method?

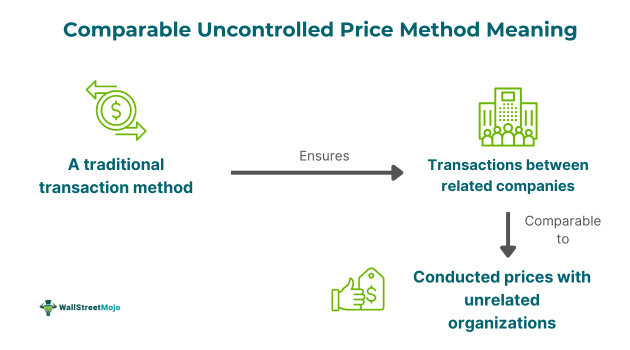

The comparable uncontrolled price (CUP) method compares the charges of the property or services of transfers in a controlled transaction to the charges of the property or services of transfers in comparable uncontrolled transactions in comparable circumstances. It is one of the five major transfer pricing methods.

The method helps determine the arm’s length pricing of cross-border transactions and the royalty of an intangible asset. It is most appropriate for commodity transactions where the same products or services are sold in both uncontrolled and controlled transactions. The products here are of the same type, quantity, and quality.

Key Takeaways

- The comparable uncontrolled price method is a pricing method that relates unrelated parties to similar prices for products or services.

- The comparison is between prices charged for products or services in controlled transactions and those of uncontrolled transactions.

- It is estimated through the use of external and internal comparable uncontrolled price methods.

- The method works best when the products between involved parties are of the same or similar characteristics.

- Its advantages include being an accurate estimation, a direct measure of arm’s length pricing, and low transfer pricing risk. Disadvantages include challenges faced in finding comparable transactions and making adjustments to the differences.

When To Use?

It can be applied in cases where there is high product comparability. The products involved shall be of the same type, nature, quantity, and quality. The transactions are required to happen at the same or similar conditions, stage of production, or distribution.

However, they can also be used in cases where there are slight product differences as long as there are no material effects on prices. If differences exist, then making adjustments to eliminate the effect would require using a different method.

Examples

Let us look at a few examples to have an understanding of the concept.

Example #1

Let’s say there is a company X that sold car parts to company Y at $5,000. X sold parts of the same nature, quantity, and quality to an unrelated party, Z, at $6,000. The transaction between X and Y is called a controlled transaction as the price is available to X. There is a difference in the transfer price.

Thus, to find the arm’s length price, adjustments have to be made. In this case, the difference for adjustment is $1,000 ($5,000-6,000), which shall be added to X’s income.

Example #2

In 2021, Latin American tax authorities increased transfer pricing audits that are related to intercompany commodity transactions. They had challenged the use of the CUP method in certain cases. They argue that it is as complex as capturing economically relevant characteristics. The recommended OECD comparable uncontrolled price method is typically suitable for commodities. Also, there are suggestions to separate spot market and future market transactions as they could have different pricing structures. It is recommended that taxpayers keep records of transaction price commodity pricing policies and document complete information with commercial and operational areas. Thus, they are useful for audit purposes

Advantages And Disadvantages

The advantages and disadvantages of the CUP method are given as follows:

Advantages

- The most accurate and has low transfer pricing risk.

- A highly recommended method of calculation of price.

- A reflection of the price agreed by two unrelated parties in relation to the transaction and hence analyzed from both ways.

- Eliminates the need and issue of involvement of related parties to be treated as the tested party with regard to pricing transfers.

- It is a direct measure of arm’s length price.

- It is less sensitive to differences in non-transfer pricing factors, which include accounting treatment differences and costs between uncontrolled and controlled parties. It can be readily used in certain transactions, such as commodity products.

Disadvantages

- It is challenging to find comparable uncontrolled transactions especially with intellectual property or services. Hence, perfect CUP is difficult to attain.

- Highly sensitive to product’s characteristic changes, which makes the application difficult.

- It is challenging to make accurate, reasonable adjustments for comparability. Differences such as markets, geography and volume, profit potential, and contract terms must be comparable.

- The adjusted differences may only sometimes have justifications or proof.

- It is hard to achieve in real life.

Frequently Asked Questions (FAQs)

How to calculate comparable uncontrolled price method?

They are calculated using the internal and external CUP methods by estimating controlled and uncontrolled transactions. Comparable uncontrolled transactions are those in which no differences between comparable transactions affect the price materially and if reasonable adjustments can be made to eliminate differences.

Is it recommended to use the CUP method?

OECD comparable uncontrolled price method is recommended to be used if the data on comparable uncontrolled transactions are available. They are considered good as they provide arm-length prices for the transactions between the parties and are better at accuracy than other methods.

What are the factors to identify while applying the CUP method?

They include geographical area, timing of transactions, the intangible properties associated with the sale, associated risks such as foreign currency risks, etc. Additionally, they include pragmatic alternatives available to sellers and buyers, contractual terms such as the date of the transactions, level of market, etc.